BREAKING: 2026 Real Estate Crash in India?

Subtitle: Or Is This the Most Overhyped Fear of the Decade?

The word is spreading fast.

Real estate crash

Real Estate Crash in India

Real Estate Crash in 2026

WhatsApp investment groups are buzzing.

YouTube analysts are predicting doom.

Investors are nervous.

And now the big question:

Will the Indian real estate market crash in 2026?

Or is this just another panic headline?

Here’s what the latest data actually tells us about 2026.

Why People Are Talking About a Real Estate Market Crash

The fear isn’t random.

- Property prices jumped 20–35% in many cities after COVID

- Home loan rates increased sharply

- EMIs became expensive

- Sales growth has slowed in 2024–2025

When prices rise too fast and demand slows, markets become vulnerable.

That’s when people start whispering:

“Is a real estate market crash next?”

Boom to Cool: What’s Really Happening in India?

Post-COVID Boom (2021–2023)

- Record residential sales in top 7 cities

- Luxury projects sold out quickly

- Low interest rates fueled buying

- Demand was massive.

Cooling Phase (2024–2025)

- Sales growth slowing

- Tier-II cities saw volume drops

- Affordability concerns rising

- Inventory is rising in some markets

This isn’t a crash signal — but it is an early warning of market stress.

Indian Real Estate - Ratio Overview

| Period | Demand | Price Trend | Market Mood |

|---|---|---|---|

| 2015–2019 | Stable | Moderate Growth | Balanced |

| 2020 | Low | Temporary Dip | Uncertain |

| 2021–2023 | Very High | Sharp Increase | Boom |

| 2024–2025 | Slowing | Growth Moderating | Cooling |

What Could Trigger a Real Estate Price Crash?

A real estate price crash doesn’t happen overnight.

It needs multiple triggers:

High Interest Rates Stay Elevated

If borrowing remains expensive, buyers step back.

Job Growth Slows

No income growth means no housing demand support.

Investor Exit

If money moves to stocks or gold, property liquidity drops.

Inventory Surge

More supply + fewer buyers = price cuts.

If all four factors occur simultaneously, the risk of a real estate price correction rises sharply.

But Here’s Why a Full Real Estate Crash in India Is Not Easy

India today is different from 2008.

- Banks are tightly regulated

- Developers are more disciplined

- RERA has improved transparency

- Demand in metro cities remains strong

A nationwide 50% collapse is unlikely without a major economic shock.

However…

Micro-markets can fall.

Luxury segments can stagnate.

Overpriced areas can correct 10–25%.

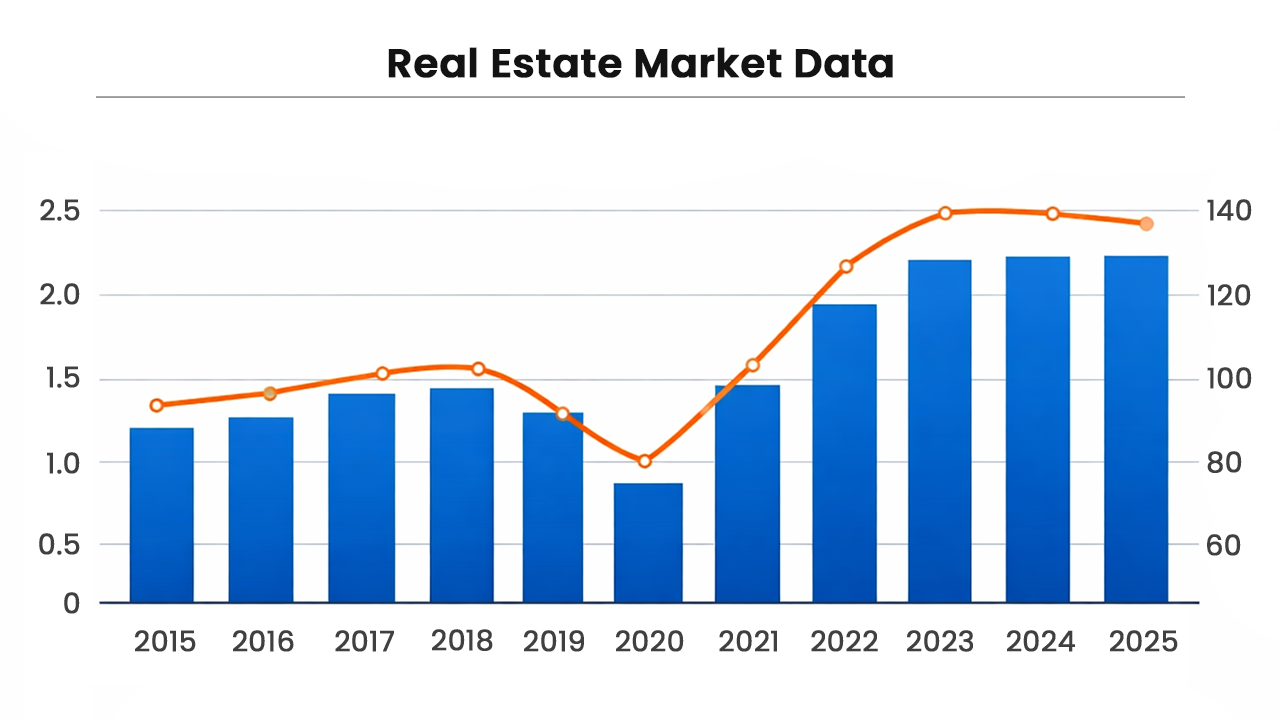

Indian Real Estate Market Data (2015–2025)

1. Residential Price Growth – 10 Year Trend

According to the National Housing Bank through its RESIDEX index:

- 2015–2019: Slow and steady growth

- 2020: Temporary dip during lockdown

- 2021–2023: Strong price surge

- 2024–2025: Growth moderating

In major cities like Mumbai, Bengaluru, and Delhi NCR, average property prices increased 20–35% between 2019 and 2024.

However, price growth in 2024–2025 slowed compared to the post-COVID boom years.

Rising prices + slower growth = early cooling signal.

2. Housing Sales Volume – Before & After COVID

Based on reports from ANAROCK and CBRE

Pre-COVID (2018–2019)

- Stable demand

- Moderate launches

- Balanced inventory

COVID Phase (2020)

- Sharp decline during lockdown

- Buyers paused decisions

Post-COVID Boom (2021–2023)

- Record sales in top 7 cities

- Low interest rates boosted buying

- Developers launched premium projects

2024–2025

- Sales growth slowed

- Tier-II cities saw around 10% drop in volume

- Unsold inventory increased in some markets

Transaction volume is softening, even if prices remain elevated.

3. Interest Rates & Affordability

The Reserve Bank of India increased repo rates between 2022 and 2023.

Higher home loan rates led to:

- Higher EMIs

- Lower first-time buyer entry

- Reduced investor leverage

Surveys show over 80% of buyers are concerned about rising prices.

Affordability pressure is growing.

4. Rental Market Surge

Prime cities saw rental increases of up to 20–25% in 2024–2025.

This shows strong urban demand.

But high rents also signal supply imbalance.

If rents stabilise or fall, property investors may hesitate.

Crash or Slowdown? What 2026 Might Look Like

Scenario 1: Mild Correction

Prices drop 10–20% in overheated cities.

Scenario 2: Time Correction

Prices stay flat for 2–3 years.

Scenario 3: Growth Continues

If supply remains tight, prices stabilise and recover.

The outcome depends on liquidity and employment strength.

Capital Rotation Between Asset Classes Is Real

If stock markets perform strongly, investors may shift money.

If economic fear increases, gold may attract capital.

Real estate competes with other asset classes.

Money flow decides direction.

Is a Real Estate Crash in India Inevitable?

A nationwide collapse looks improbable at this stage — but selective corrections are increasingly part of the 2026 conversation.

Sales Momentum Is Cooling

Housing sales across India’s top seven cities declined about 14% in 2025, falling from roughly 4.6 lakh units to 3.9 lakh units. However, the total transaction value rose nearly 6%, indicating continued demand in higher-priced segments.

This reflects moderation, not distress.

Inventory Build-Up Remains Controlled

Unsold inventory increased around 4% to nearly 5.77 lakh units. While rising supply alongside slower sales creates pressure, the increase remains gradual rather than alarming.

Price Growth Is Slowing, Not Collapsing

Property prices across major cities grew roughly 8% year-on-year in 2025, slower than the sharp post-COVID surge (Economic Times).

Delhi NCR saw the highest jump at around 23%, mainly driven by luxury projects (Economic Times).

Slower growth is different from falling prices.

Right now, we are seeing deceleration, not a real estate price crash.

City-wise Real Estate Crash Analysis - 2026

| City | 2025 Price Trend | Inventory Trend | Demand Strength | 2026 Crash Risk Level | Key Risk Factors | Data Source |

|---|---|---|---|---|---|---|

| Mumbai | Moderate growth | Large but stable inventory | Strong luxury demand | Medium | High prices, affordability stress | (Economic Times – ANAROCK Inventory Report) |

| Delhi NCR | ~23% price rise (highest among metros) | Inventory rising | Premium demand strong | Medium–High | Rapid price spike + rising supply | (Economic Times – Housing Sales & Price Report) |

| Bengaluru | Steady growth | ~23% rise in unsold stock | Strong IT-driven demand | Medium | Peripheral oversupply risk | (Economic Times – Inventory Analysis) |

| Pune | Slowing price growth | Moderate inventory increase | Balanced but cooling | Medium | Outer suburb supply pressure | (Economic Times – ANAROCK Report) |

| Hyderabad | Stable growth | Balanced / slight improvement | Healthy absorption | Low–Medium | Luxury segment sensitivity | (Economic Times – Sales Value Report) |

| Ahmedabad | Steady, affordable growth | Controlled supply | Stable local demand | Low–Medium | Credit tightening risk | (Economic Times – Market Coverage) |

India’s real estate market is highly localised. While Delhi NCR and select micro-markets show elevated correction risk due to rapid price growth and rising inventory, cities like Hyderabad and Ahmedabad appear more stable.

A nationwide real estate crash in 2026 looks unlikely based on current supply-demand data, but localised corrections of 10–25% remain possible in overheated pockets.

Comparison With the 2008 Global Crash

Many people compare 2026 fears with the 2008 global housing crash.

But the structures are very different.

Why India Didn’t Collapse Like the US in 2008

In 2008, the US crisis was triggered by subprime lending and risky mortgage-backed securities. India did not have large-scale toxic mortgage exposure.

Indian home loans have traditionally required stronger income verification and lower risk structures.

This limited systemic damage.

Stronger Regulation Today: RERA

The Real Estate (Regulation and Development) Act, 2016 (RERA) improved transparency, escrow norms, and buyer protection (Wikipedia – RERA overview).

Developers must register projects and maintain financial discipline.

This reduces the risk of speculative bubbles spiralling out of control.

Banking System Safeguards

Indian banks operate under stricter capital adequacy norms compared to the US pre-2008 system.

Lending standards are more conservative. There is no widespread subprime-style leverage today. This significantly lowers the probability of a nationwide collapse.

Strategic Investing During Uncertain Markets

Weak projects suffer first. Overleveraged developers struggle. Speculative launches freeze. But strong fundamentals survive.

Location quality. Demand-driven pricing. Phased inventory release. Financial discipline.

These factors protect investments during volatility.

In such an environment, project selection becomes more important than market timing. Investors increasingly prioritise developers with disciplined execution and demand-driven strategies.

Why Investors Are Choosing Laxmi Group During Market Uncertainty

In times when headlines scream “real estate crash in 2026”, smart investors shift their focus from hype to fundamentals — particularly when considering investment in Ahmedabad and other stable growth corridors.

This is where Laxmi Group stands out.

Strategic Location Selection

Laxmi Group focuses on growth corridors and infrastructure-backed micro-markets rather than speculative hotspots.

This reduces correction risk even during market slowdowns.

Strong Project Planning & Execution

Both Residential Projects and Commercial Projects are aligned with real demand. Inventory is launched in phases.

This prevents oversupply pressure.

Transparent Pricing & Compliance

With strict regulatory frameworks like RERA in place, Laxmi Group maintains compliance, transparency, and timely delivery.

This builds long-term buyer confidence — especially during cooling cycles.

Focus on End-User Demand

Unlike speculative luxury bubbles, projects are aligned with practical affordability segments.

And in uncertain markets, end-user demand is the real backbone.

Your Questions, Honest Answers

Is the Indian real estate market going to crash in 2026?

A nationwide crash looks unlikely. The market is slowing, not collapsing. Some local corrections may happen.

Will property prices fall in India in 2026?

Prices may correct in overheated areas. Luxury markets face higher risk. Most cities may see stability instead of sharp falls.

What are the signs of a real estate slowdown?

Sales growth is moderating. Inventory is rising slowly. Price growth is easing. These signal cooling, not a crash.

Should I wait to buy property in 2026?

It depends on your goal. End-users can buy based on need. Investors may wait for clearer price signals.

What could trigger a real estate crash in India?

High interest rates. Job losses. Credit stress. Rapid oversupply. All must occur together for a crash.

Which cities are most at risk in 2026?

Cities with sharp recent price spikes face higher risk. Markets with rising inventory need caution. Risk is local, not nationwide.

How do interest rates affect housing prices?

Higher rates increase EMIs. Demand weakens. Lower rates improve affordability. Buying activity rises.

What is the difference between a slowdown and a crash?

A slowdown means slower growth. Prices stabilise. A crash means sharp price drops and distress selling.

Is 2026 similar to the 2008 housing crisis?

No. Lending rules are stricter today. Banks are better regulated. Systemic risk is lower.

What should investors focus on now?

Strong locations. Real demand. Controlled supply. Financial discipline. Avoid speculation.